Abstract Of KSA PDPL – Article 24

This paper presents a comprehensive overview of the necessary controls and procedures required for the lawful processing of credit data, as outlined in Article 24 of the Kingdom of Saudi Arabia’s Personal Data Protection Law (KSA PDPL) and the Credit Information Law. It highlights key strategic points, compliance challenges, and enablement methodologies to ensure the privacy of data subjects, protect their rights, and align with legal mandates. The paper further explores practical use cases, dependencies, risks, and technologies associated with effective credit data governance.

Keywords

Credit Data; Personal Data; KSA PDPL; Credit Information Law; Data Subject Privacy; Explicit Consent; Disclosure Control; Data Governance

Introduction Of KSA PDPL – Article 24

In the era of digital transformation, the handling of personal data, especially credit data, has become more sensitive and regulated. As part of the Kingdom of Saudi Arabia’s Personal Data Protection Law (PDPL) and the Credit Information Law, Article 24 mandates the creation of additional controls for processing credit data. These controls are designed to preserve the privacy of data subjects and ensure their rights are protected. This paper digs into and explores Article 24, outlining strategic approaches to ensure compliance and practical application within organizations handling credit data.

Explanation Of KSA PDPL – Article 24

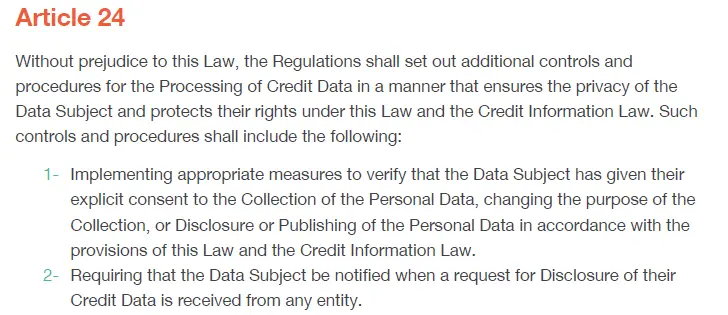

Article 24 emphasizes the need for specific controls and procedures to ensure credit data processing aligns with privacy and data protection laws. It requires data controllers to secure explicit consent from data subjects for the collection, disclosure, or publication of their personal data and notify them if a third party requests access to their credit data. These measures aim to safeguard individuals’ privacy and ensure their personal information is not misused.

Key Strategic Points

- Explicit Consent Mechanisms: Establishing strong procedures to secure and verify the data subject’s explicit consent for processing activities, such as collection or changes in data usage, is critical.

- Purpose Limitation: Data controllers should ensure that personal data is processed only for the original purpose for which consent was obtained, as per KSA PDPL and the Credit Information Law.

- Transparency in Data Disclosure: Data subjects must be informed when third-party entities request their credit data to maintain transparency and trust.

- Regulatory Compliance: Aligning all credit data processing activities with both the KSA PDPL and the Credit Information Law to avoid legal penalties and maintain consumer trust.

General Activation Steps

- Establish Consent Management Processes: Implement systems for obtaining, recording, and verifying explicit consent for data collection and usage.

- Notify Data Subjects of Disclosure Requests: Create notification workflows to inform data subjects whenever their credit data is requested by a third party.

- Data Processing Audits: Regularly audit data processing activities to ensure alignment with legal provisions.

- Train Staff on Legal Compliance: Ensure that all employees handling personal and credit data are trained in compliance with KSA PDPL and Credit Information Law.

Enablement Methodology

To enable organizations to meet the requirements of Article 24, the following steps should be incorporated:

- Technological Integration: Leverage consent management platforms and data governance tools to automate consent collection, storage, and verification.

- Legal Consultation and Audit: Engage with legal experts to ensure the organization’s data processing strategies comply with national laws and international best practices.

- Awareness Campaigns: Educate stakeholders, including data subjects, about their rights and the organization’s obligations under the law.

Use Cases

- Financial Institutions: Banks and credit agencies using customer data must implement robust mechanisms for collecting and storing explicit consent before processing credit data.

- Credit Bureaus: They must notify individuals when their credit data is requested by a third party, maintaining transparency and building trust.

- Fintech Companies: Companies handling large volumes of customer financial data must integrate privacy-by-design principles into their systems to meet regulatory requirements.

Dependencies

- Compliance with Credit Information Law: Companies must ensure their processing activities are in accordance with the specific provisions of the Credit Information Law.

- Technological Infrastructure: Adequate technology platforms to manage data consent, privacy, and notification procedures.

- Organizational Readiness: Staff should be prepared through continuous education and training on privacy laws and data protection measures.

Tools/Technologies

- Consent Management Platforms: Solutions like OneTrust, TrustArc, or custom-built platforms to manage data subject consent.

- Data Governance Tools: Technologies such as Collibra or Informatica for managing and auditing data processes.

- Notification Systems: Automated notification systems to inform data subjects about disclosure requests in real time.

Challenges & Risks Of KSA PDPL – Article 24

- Failure to Obtain Explicit Consent: Non-compliance in obtaining explicit consent can result in legal penalties, reputational damage, and loss of consumer trust.

- Insufficient Notification Mechanisms: Inadequate systems for notifying data subjects about third-party requests could lead to breaches of Article 24.

- Technological Barriers: Implementing and maintaining the required technological infrastructure can be challenging, especially for smaller organizations with limited resources.

- Legal and Compliance Risks: Organizations face the risk of non-compliance with the evolving landscape of privacy laws, which requires continuous monitoring and adaptation.

Conclusion

The implementation of Article 24 of the KSA PDPL and the Credit Information Law is a critical step in safeguarding the privacy of credit data subjects. By establishing strong consent management processes, ensuring transparency in data disclosure, and aligning with the legal framework, organizations can protect individuals’ rights and build trust. Although there are challenges in compliance, proper planning, technology adoption, and training will enable successful implementation.

References

- KSA Personal Data Protection Law (PDPL), Article 24.

- Saudi Credit Information Law.

- NDMO Guidelines on Data Privacy and Protection.

Recommended Resources:

- Big Data vs. Traditional Data, Data Warehousing, AI, and Beyond

- Big Data Security, Privacy, and Protection, & Addressing the Challenges of Big Data

- Designing Big Data Infrastructure and Modeling

- Leveraging Big Data through NoSQL Databases

- Data Strategy vs. Data Platform Strategy

- ABAC – Attribute-Based Access Control

- Consequences of Personal Data Breaches

- KSA PDPL (Personal Data Protection Law) – Initial Framework

- KSA PDPL – Consent Not Mandatory

- KSA PDPL Article 4, 5, 6, 7, 8, 9, 10, 11, & 12

- KSA PDPL Article 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, & 23

- KSA NDMO – Data Catalog and Metadata

- KSA NDMO – Personal Data Protection – Initial Assessment

- KSA NDMO – DG Artifacts Control – Data Management Issue Tracking Register

- KSA NDMO – Personal Data Protection – PDP Plan, & PDP Training, Data Breach Notification

- KSA NDMO – Classification Process, Data Breach Management, & Data Subject Rights

- KSA NDMO – Privacy Notice and Consent Management

- Enterprise Architecture Governance & TOGAF – Components

- Enterprise Architecture & Architecture Framework

- TOGAF – ADM (Architecture Development Method) vs. Enterprise Continuum

- TOGAF – Architecture Content Framework

- TOGAF – ADM Features & Phases

- Data Security Standards

- Data Steward – Stewardship Activities

- Data Modeling – Metrics and Checklist

- How to Measure the Value of Data

- What is Content and Content Management?